/cloudfront-us-east-2.images.arcpublishing.com/reuters/P5ILWRK3J5JTPP6NIVPY7Y7P7U.jpg)

Brookfield Real Assets: Great yield play but historically high premium (NYSE: RA)

nespix/iStock via Getty Images

Investment thesis

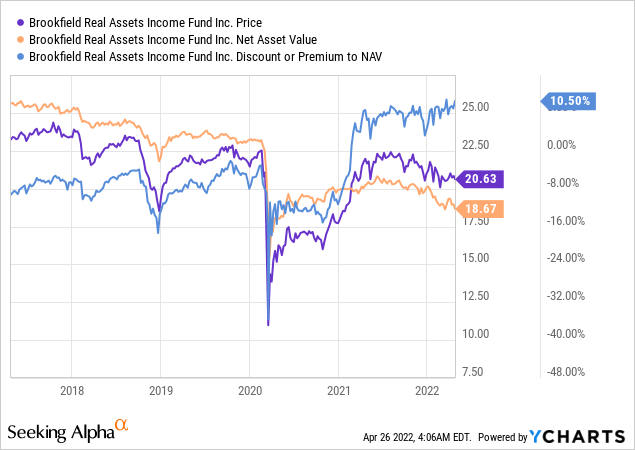

Brookfield Real Assets Income Fund (NYSE:NYSE:RA) is down 5.6% in the previous 52 weeks and 2.7% since the start of the year. However, being a high yield income game, its real essence lies in its distributions, and share price performance should only be used to assess an entry point into the CEF.

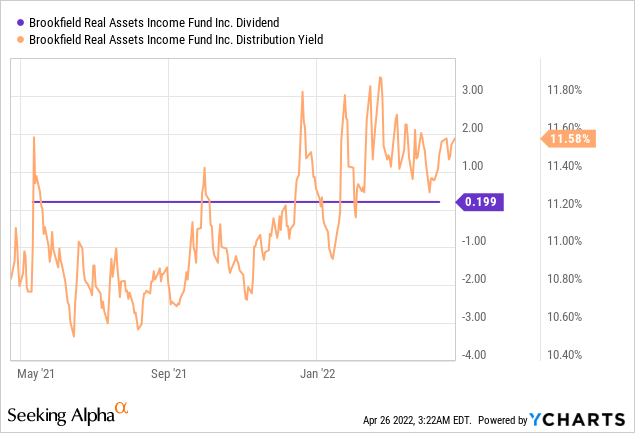

A lower price is often an indication of better valuations for potential investors. Historically, the fund has always traded at a discount to pre-February 2021 NAV. Yet despite trading below its 52-week average market price of $21.52, the fund is currently trading at a premium to net asset value of 10.5%, close to its 52-week net asset value. up to 10.81%.

The company’s monthly dividend policy of $0.199 per share offers an attractive 11.5% annualized return to price and a 12.8% return to NAV. A significant portion of the company’s distributions was a return on capital, with 71.54% in 2020 and 61.57% in 2021, which can be used as a tax benefit but can also indicate net asset value depletion, calling into question question future distribution sustainability issues.

Although trading at a historically high premium, the fund’s moderate leverage makes it a suitable option for both bull and bear markets. Nonetheless, rising interest rates will put further pressure on the company’s net income, meaning that a significant portion of distributions will likely still be made in the form of return of capital.

Regular investors may still find the fund attractive to invest in due to its distributions and combination of leverage. Nevertheless, new investors should be wary of plunging into such premiums and rising return on capital. A better entry point is likely to open up the road; until then, I am neutral on the title.

The bottom

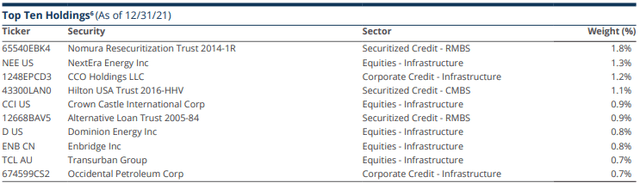

RA is a closed-end fund that began operations in December 2016, investing primarily in securities and instruments it calls “real assets,” including real estate, infrastructure and natural resource securities. 37.8% of its assets are equity-based instruments, 35.7% are corporate loans and 28.5% are securitized loans divided between RMBS, CMBS and other real estate securities. 69% of its securities are fixed rate and 31% variable rate.

Brookfield Real Assets Income Fund

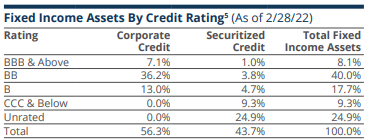

The bulk of the fund’s income portfolio is allocated to a class of high-risk debt securities issued by infrastructure and real estate companies. Only 8.1% of its assets are classified investment grade instruments. Its high-yield, high-risk instruments are generally not suitable for individual investors due to the high-risk exposure they bring to the table.

Brookfield Real Assets Income Fund

Premium/discount and interest rate hike

CEFs are better suited to be part of your investment portfolio as a vehicle to fill different asset classes rather than being considered an asset class themselves. Indeed, they cannot be fully generalized as a class without considering the risk-return profile of their portfolios held, adding an advantage to investors who wish to invest in a portfolio of securities with varying degrees of risk and reward.

Demand for the asset classes held in a CEF portfolio is a determining factor in determining the premium or discount to net asset value. This demand is often correlated to the interrelationship of an asset class with interest rates. A rising interest rate environment is likely to increase the market price of CEF’s Interest Rate Linked Portfolio faster than its net asset value, resulting in high premiums to net asset value.

In a recovering post-pandemic economy, higher interest rates had been expected since early 2021, which may have been a crucial factor in Brookfield’s sudden trading shift from a discount to a premium. Given that rising interest rates are expected to continue through 2023, the premium to RA’s net asset value is likely to continue. Nevertheless, it will be subject to high volatility based on other factors, such as the trading volume/liquidity of its shares.

Brookfield has adequate leverage

The degree of leverage in a CEF dictates above-market returns by exposing the business to varying degrees of risk. Regardless of the source of leverage, the objectives and effects are mostly similar; for example, increasing leverage increases returns. The higher risk exposure also leads to higher volatility in the net asset value and market price of a CEF. I have tried to highlight these two factors through the following tables:

| Leverage on return | CEF without leverage | Brookfield Real Assets | High Leverage CEF |

| Outstanding shares | 50,098,295 | 50,098,295 | 50,098,295 |

| NAV | 935,335,000 | 935,335,000 | 935,335,000 |

| Leverage | 0 | 404,957,000 | 935,500,000 |

| Total assets | 935,335,000 | 1,340,292,000 | 1,870,835,000 |

| Leverage ratio | 0.00% | 30.21% | 50.00% |

| Total investment income | 39,097,003 | 56,018,065 | 78 200 903 |

| Effective income rate on total assets | 4.18% | 4.18% | 4.18% |

| Borrowing costs | 0 | 2,540,004 | 5,893,650 |

| Effective borrowing rate | 0.63% | 0.63% | 0.63% |

| Net investment income | 39,097,003 | 53,478,061 | 72 307 253 |

| Yield on NAV | 4.18% | 5.72% | 7.73% |

Source: Author

I used the actual total investment income from RA’s financial statements and used it to stipulate an effective income rate and ignored all other expenses to isolate the actual borrowing expenses and extract an effective borrowing rate as a percentage of actual current leverage. As can be seen, higher leverage leads to higher returns. A nearly 20% increase in leverage from 30.21% to 50% increases the effective return on net asset value by more than 35%. However, as we will see below, this will also lead to a higher risk.

| Potential effect on net asset value if the market falls by 10% | CEF without leverage | Brookfield Real Assets | High Leverage CEF |

| NAV per share | 18.67 | 18.67 | 18.67 |

| Leverage | 0 | 404,957,000 | 935,500,000 |

| Total assets | 935,335,000 | 1,340,292,000 | 1,870,835,000 |

| Leverage ratio | 0.00% | 30.21% | 50.00% |

| Total assets after 10% market decline | 841 801 500 | 1,206,262,800 | 1,683,751,500 |

| Minus: leverage | 0 | 404,957,000 | 935,500,000 |

| NAV after market decline | 841 801 500 | 801 305 800 | 748 251 500 |

| Leverage after decline | 0% | 50.53% | 125% |

| NAV per share after decline | 16.80 | 15.99 | 14.94 |

| Net decrease in net asset value per share | 10.00% | 14.33% | 20.00% |

Source: Author

In the event of a 10% decline in the market value of the fund’s total assets, its net decline in net asset value is greater than that of a low-leverage company due to a combination of higher leverage in its portfolio. Again, the nearly 20% increase in leverage, from 30.21% to 50%, results in a nearly 40% net decline in net asset value per share from 14.33% to 20 %.

Moreover, since the amount borrowed remains unchanged, the effective leverage after a fall in the net asset value increases to higher levels, further increasing the effective exposure, which more than doubles in our high-effect scenario. of leverage.

Moreover, leverage also affects performance in a market where interest rates change.

| Effect of a 25 basis point change in interest rates | Brookfield | Rising interest rates | Decreasing interest rate |

| NAV | 935,335,000 | 935,335,000 | 935,335,000 |

| Leverage (30.21%) | 404,957,000 | 404,957,000 | 404,957,000 |

| Total assets | 1,340,292,000 | 1,340,292,000 | 1,340,292,000 |

| Total investment income | 56,018,065 | 56,018,065 | 56,018,065 |

| Effective borrowing rate | 0.61% | 0.86% | 0.36% |

| Borrowing cost | 2,470,238 | 3,482,630 | 1,457,845 |

| Net investment income | 53,547,827 | 52 535 435 | 54 560 220 |

| Yield on NAV | 5.73% | 5.62% | 5.83% |

Source: Author

In the event of an increase in the effective borrowing rate of 25 basis points, the yield of the ANAV falls by almost 200 basis points from 5.73% to 5.62%, exposing the risks of the situation current macroeconomics.

Typically, high-leverage funds outperform low-leverage companies in a bull market and underperform in a bear market. Brookfield is moderately leveraged at around 30%, meaning the company is poised to perform adequately in either market.

Distributions

The fund has a payout yield of well over 11%, but with the exception of 2017 and 2018, the company has mostly performed in a near-zero interest rate environment since inception. The current environment is marked by high inflation and rising interest rates, leading to generic risks for CEFs that will test the resilience of AR revenues.

The company’s monthly distribution of $0.199 has remained unchanged since its inception, but the previous 2 years’ dividends have been heavily dependent on return of capital, which is not a good sign for the company’s long-term health. an EFC due to the erosion of the net asset value.

RA is a good source of reliable income for its investors, but current circumstances are less than ideal for potential investors looking for a long-term income stream. Any improvement would need to be watched closely as I believe the company holds positive value and is likely to increase its earnings to avoid erosion of the net asset value based on the underlying value of its securities.

Conclusion

CEFs are complex vehicles, and investors should only dive into them after reviewing their underlying portfolios. Depending on an investor’s risk appetite, one should carefully select the type of FEC in which he wishes to invest based on its risk/return ratio.

RA offers a healthy mix of portfolios producing over 11% monthly distributions. Under general circumstances, CEF would certainly be a buy, but current valuation metrics should decline in the coming months, providing a better entry point for potential investors. Potential investors are better off holding their positions until the premium drops, maximizing the gain.

Arguably, a one-time premium of 10.5% is worth the perpetual return, but first, based on the high return on capital, “perpetual” is a big leap forward. Second, a premium nearly equal to the annual return means the capital would be better spent elsewhere, generating meaningful returns.